Credit Score-

One of the easiest ways to accrue a pile of miles is through credit card sign-up bonuses. In fact it is common to see 50,000 mile offers and higher for signing up for a new credit card; 100k BA Chase (expired), 100k Chase Sapphire Preferred (live), 150k AA miles (live). Before you go into this world of credit card bonuses it is necessary to understand Credit. You need to use your intelligence about your credit and avoiding taking on more risk than you can handle. If you can learn the fundamentals of the credit card game you will see it is the most rewarding bonus mileage program.

The first thing you must be diligent with is your credit score. Your credit score, known as a FICO score, is the aggregate of all credit data that can be gathered on you. It is called a FICO because the company that gathers, packages and sells this information about your credit is FICO. FICO scores can range from 300-850, the higher the better, with an average FICO score between 700-725 for 2011.

I do not like to use generalizations, but as long as you can maintain a FICO of 725 or higher you should not have any problems with your applications. Of course you have to take this with a grain of salt, evaluate every promo offer and decide whether you are an ideal candidate before applying.

Credit Data-

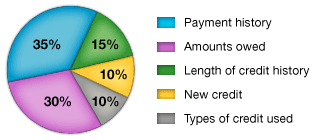

The pie graph shown below is the breakdown of how your credit score is built. Each data category is given a percent value of how important it is to the composition of your FICO.

For example, according to the Pie graph 65% of your FICO can be traced back to the Payment History and Amounts Owed category's.

Credit Data as % Value of Importance, image from MyFICO.

The graph is from MyFICO.com which has tons of FREE information under their "education" tab to help you.

For a quick crash course start with these articles:

- Credit Score Facts & Fallacies

- What's in your FICO® score

- What's NOT in your FICO® score

- Improving your Score

From here you can explore the site yourself. Remember to never apply for credit cards or other credit dependent obligations without first understanding the conditions.

There are three different Credit Reporting Agency's in the United States and all three give you a different FICO score. You should check if there are any errors on your credit report which, you can obtain for free every 12 months from AnnualCreditReport.com. I would also recommend the credit database websites of whogavemecredit.com and creditboards.com to find out what lenders use which credit bureaus in your state (U.S.).

References-

There are also two sites that I found to be extremely helpful with not only this particular topic but many; thefrugaltravelguy.com and thepointsguy.com. They are both long time veterans of this mileage/points game and they always have top quality content, so go check them out.

I do not get compensated or work for MyFICO or any subsidiaries of MyFICO. I am not authorized to speak on their behalf. I simply think their articles on credit scores are comprehensive, easy to read and FREE are the best out there.

No comments:

Post a Comment